Investing can be a powerful tool for building long-term wealth, but with so many options available, it’s easy to get overwhelmed—especially when choosing between index funds and actively managed funds. These two approaches dominate the world of mutual funds and ETFs, and understanding the difference between them is essential for anyone serious about investing smartly.

In this comprehensive guide, we’ll dive deep into what each type of fund offers, how they differ in terms of performance, fees, risks, and transparency, and which one might be better suited for your financial goals.

Understanding the Basics

What Are Index Funds?

An index fund is a type of passive investment vehicle that aims to replicate the performance of a specific financial market index, such as the S&P 500, Nasdaq-100, MSCI World, or Brazil’s Ibovespa. Instead of trying to beat the market, an index fund simply mirrors it.

The portfolio of an index fund typically includes all—or a representative sample—of the securities in the underlying index in the same proportions. Since there’s no active decision-making, the fund requires less management, which translates into lower fees and lower portfolio turnover.

What Are Actively Managed Funds?

In contrast, an actively managed fund is run by a portfolio manager or investment team who actively selects investments in an attempt to outperform a benchmark index. These funds are constantly adjusted based on market research, economic forecasts, and individual company analysis.

Because of this hands-on management, actively managed funds generally come with higher fees, more frequent trading, and the possibility of outperforming the index—or underperforming it.

Key Differences Between Index Funds and Actively Managed Funds

Let’s break down the primary differences between the two:

| Feature | Index Funds | Actively Managed Funds |

|---|---|---|

| Objective | Match market returns | Beat market returns |

| Fees | Low (often < 0.10%) | High (0.50%–2% or more) |

| Management | Passive | Active |

| Performance | Matches the index | Varies—may outperform or underperform |

| Transparency | High | Often lower |

| Tax efficiency | High | Lower (due to more trading) |

| Risk | Market risk | Market + manager risk |

Cost Comparison: Why Fees Matter So Much

One of the most compelling reasons many investors prefer index funds is the cost advantage.

Expense Ratios

An index fund may charge as little as 0.03% to 0.10% annually. For example, investing R$100,000 in an index fund with a 0.05% expense ratio would cost just R$50 per year.

By contrast, many actively managed funds charge between 1% and 2% annually. That same R$100,000 investment could cost R$1,000 to R$2,000 per year in fees. Over a period of 20–30 years, these costs can add up to tens of thousands of reais in lost returns.

The Compounding Effect of Fees

Imagine two investors each putting R$50,000 into separate funds over 25 years with an average return of 8%:

- Index Fund (0.10% fee): Final value ≈ R$329,000

- Active Fund (1.00% fee): Final value ≈ R$289,000

That’s a R$40,000 difference due to fees alone.

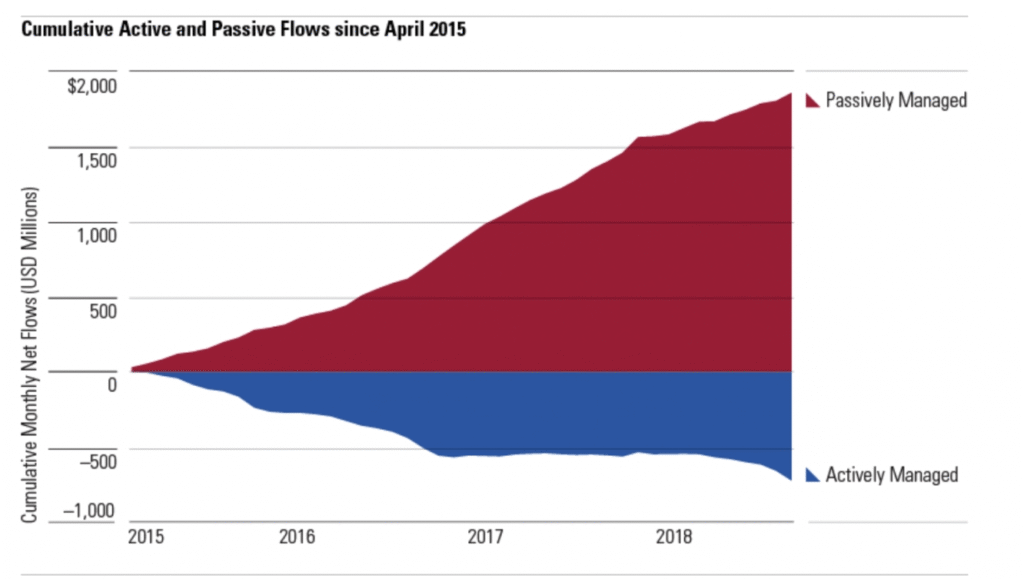

Historical Performance: The Numbers Don’t Lie

Most investors assume that if they pay more for a skilled fund manager, they’ll earn better returns. Unfortunately, this is not always the case.

SPIVA Data

The S&P Indices Versus Active (SPIVA) report regularly compares the performance of actively managed funds to their respective benchmarks. The results are revealing:

- Over a 10-year period, 85%–90% of large-cap active funds underperform the S&P 500.

- In Brazil, the percentage of funds that underperform the Ibovespa is also very high over long periods.

- The longer the time frame, the more index funds outperform.

While some active managers do beat the market over certain years, very few do it consistently, and choosing them in advance is extremely difficult.

Risk: Different Profiles for Different Investors

Index Funds

Index funds carry market risk, meaning if the market goes down, so does your investment. However, they usually have broad diversification and no single decision can drastically impact the fund’s performance.

Their passive nature means they won’t try to avoid losses or shift strategies—so during a downturn, index investors are along for the ride.

Actively Managed Funds

These funds may be more volatile, depending on the manager’s strategy. A manager may concentrate holdings in a few companies, increasing both upside potential and downside risk.

Some managers may try to reduce risk during downturns by shifting assets to bonds or defensive sectors. However, this relies on the ability to time the market correctly—something very few managers do consistently.

Transparency and Control

With index funds, you know exactly what you’re investing in. The holdings mirror a known index and are publicly disclosed.

Actively managed funds can be more opaque. They may not disclose their current holdings as frequently, and they can shift strategies depending on market conditions, making them harder to track.

Tax Efficiency

Index Funds:

- Lower turnover = fewer taxable events

- More suitable for long-term investing in taxable accounts

Actively Managed Funds:

- Frequent buying and selling can generate capital gains, which may be passed on to investors.

- Less tax-efficient overall, unless held in a tax-deferred account like a previdência privada.

When Index Funds Might Be Better

Index funds are often better for:

- Long-term investors seeking steady growth

- Those with a buy-and-hold strategy

- Investors looking for low fees and simplicity

- People who believe in the efficient market hypothesis

- Beginners who want a set-it-and-forget-it portfolio

When Actively Managed Funds Might Be Better

While most investors benefit from index funds, active management may be worthwhile in certain scenarios:

- Niche markets: In less efficient markets (e.g., emerging markets, small caps), active managers may have an edge.

- Income strategies: Funds focused on dividends, covered calls, or fixed-income securities may benefit from active research.

- Tactical allocation: Some investors want managers who can adjust the portfolio based on macroeconomic trends or risks.

- Absolute return focus: Certain hedge funds or long-short strategies seek to deliver returns regardless of market conditions.

Blending Both Approaches: Core-Satellite Strategy

A balanced approach is to use a core-satellite strategy, where:

- The core (70–90%) of the portfolio consists of index funds for low-cost, broad exposure.

- The satellite (10–30%) includes actively managed funds for diversification or potential alpha.

This strategy provides the benefits of cost efficiency, diversification, and some active opportunities.

Real-World Example

Let’s say you have R$100,000 to invest.

- You put R$80,000 in index funds tracking the B3, S&P 500, and global markets.

- The remaining R$20,000 goes to active funds focused on small-cap Brazilian companies and emerging market debt.

This portfolio is well-diversified, cost-effective, and has the potential to outperform the market without excessive risk.

Choosing the Right Fund for You

Here are some key questions to ask before deciding:

- What are my investment goals?

- Retirement? Passive income? Short-term growth?

- What’s my risk tolerance?

- Am I comfortable with volatility, or do I prefer stability?

- How involved do I want to be?

- Do I want to research managers or go with a passive strategy?

- Am I investing in a taxable account?

- If so, index funds may be more tax-efficient.

- Do I believe in beating the market?

- Or am I satisfied with market-matching returns?

Final Thoughts

The decision between index funds and actively managed funds isn’t a binary one. For most investors—especially beginners—index funds offer the best combination of performance, cost-efficiency, and simplicity. They take the guesswork out of investing and let you participate in the growth of the market.

However, there are cases where active management adds value, particularly in niche areas, tactical strategies, or when managed by an exceptional team.

Ultimately, the best strategy is the one that aligns with your goals, time horizon, and risk profile. Whether you go passive, active, or a mix of both, consistency and discipline will matter more than anything else.