When it comes to investing, one of the most debated topics is the choice between index funds and actively managed funds. For beginner and even intermediate investors, understanding the difference between these two strategies is critical to building an effective portfolio. Each has its own pros and cons, and the right choice depends on your goals, risk tolerance, and investment philosophy.

In this article, we’ll explain what each type of fund is, how they work, their historical performance, fees, and which might be better for your investment journey.

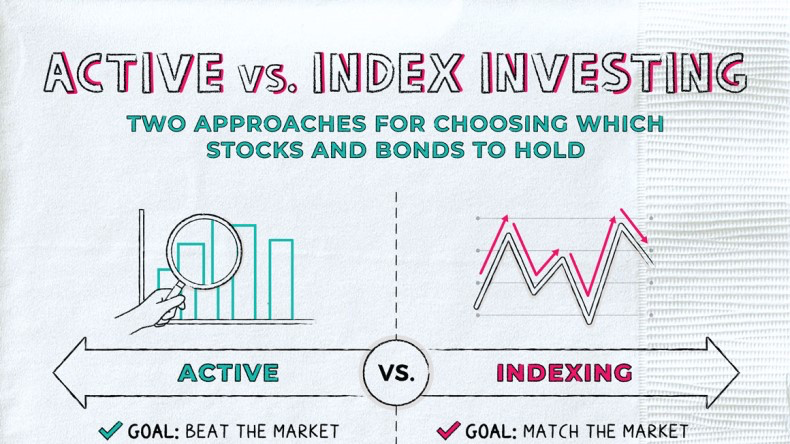

What Are Index Funds?

Index funds are a type of mutual fund or exchange-traded fund (ETF) that aims to replicate the performance of a specific market index, such as the S&P 500, Ibovespa, Nasdaq, or others.

Instead of trying to “beat the market,” an index fund simply tries to match the market. That means if the index goes up 10%, the fund should also rise by about 10% (minus small fees).

How Index Funds Work

Index funds hold a representative basket of securities in the same proportion as the underlying index. For example:

- The IVVB11 ETF in Brazil tracks the S&P 500, giving you exposure to 500 top U.S. companies.

- The BOVA11 ETF tracks the Ibovespa, giving you exposure to major Brazilian stocks.

What Are Actively Managed Funds?

Actively managed funds are overseen by a professional fund manager or a team of analysts who make decisions on what securities to buy, hold, or sell in an attempt to outperform the market or a specific benchmark.

Instead of tracking an index, these funds are built based on the manager’s analysis, experience, and market views.

Examples of actively managed funds include:

- Hedge funds

- Mutual funds with a specific strategy

- Specialized equity or fixed-income funds

Key Differences Between Index Funds and Actively Managed Funds

| Feature | Index Funds | Actively Managed Funds |

|---|---|---|

| Strategy | Passive – tracks an index | Active – aims to beat the market |

| Fees | Low (as little as 0.03% per year) | High (can exceed 2% per year) |

| Manager Involvement | Minimal | High |

| Performance | Matches index (minus fees) | Can outperform or underperform |

| Transparency | High – follows public index | Moderate – depends on disclosure |

| Risk | Market risk | Market + manager risk |

Pros and Cons of Index Funds

✅ Pros

- Low Cost

Index funds have very low management fees, which means more of your returns stay in your pocket. - Diversification

A single fund can give you exposure to hundreds of stocks across industries. - Transparency

You know exactly what you’re getting because the index is public. - Outperformance of Active Funds (on average)

Studies consistently show that most actively managed funds fail to beat their benchmark over the long term. - Ideal for Long-Term Investors

Perfect for those who want to invest consistently without timing the market.

❌ Cons

- No Flexibility in Down Markets

Index funds follow the market — if the index falls, so does your investment. - No Chance of Outperformance

Index funds are guaranteed to never outperform the market.

Pros and Cons of Actively Managed Funds

✅ Pros

- Potential to Beat the Market

Skilled managers can deliver above-average returns during certain market conditions. - Downside Protection

Managers can move to cash or defensive positions during downturns. - Tactical Allocation

Ability to shift between sectors or asset classes based on market conditions. - Access to Niche Markets

Active funds may invest in opportunities that indexes can’t — like small, illiquid, or emerging market securities.

❌ Cons

- High Fees

Many active funds charge 2% or more annually, plus performance fees. - Inconsistent Performance

Even the best managers can underperform — and many do. - Manager Risk

Your investment is tied to the decisions of a specific individual or team. - Lack of Transparency

You may not always know exactly what the fund is holding or why.

Historical Performance: What Do the Studies Show?

Multiple studies have evaluated the performance of active versus passive funds, and the results are clear:

- Over 80% of actively managed funds underperform their benchmarks over the long term.

- The SPIVA report (S&P Indices Versus Active) consistently shows that passive funds outperform active ones in most categories over a 10- to 20-year period.

- In Brazil, although there are some exceptions, many multimercado and equity funds also struggle to beat the CDI or Ibovespa consistently, especially after fees.

That said, a small minority of active managers do outperform — but they are difficult to identify in advance.

Fee Comparison: A Silent Killer of Returns

Let’s look at how fees impact your investment:

- Assume you invest R$10,000 at a 7% annual return over 30 years.

- Index fund with 0.2% fee: Final amount = R$74,000

- Active fund with 2% fee: Final amount = R$57,000

That’s a R$17,000 difference — just in fees.

When to Choose Index Funds

Index funds are great if:

- You’re a beginner investor

- You prefer low-cost, diversified exposure

- You’re investing for retirement or the long term

- You don’t want to actively manage your investments

They work best in efficient markets (like large-cap U.S. stocks), where it’s very hard for active managers to add value.

When to Consider Actively Managed Funds

Active funds can make sense if:

- You want exposure to niche areas (emerging markets, distressed assets, small-cap value)

- You believe in a specific manager or strategy

- You’re okay with higher fees for the potential of higher returns

- You want tactical allocation or downside protection

Also, during volatile or falling markets, skilled active managers may protect your capital better than an index.

What About a Blend of Both?

Many investors choose to combine index and active funds in their portfolios. This approach can provide:

- Cost efficiency (via index funds)

- Potential alpha (via active funds)

- Exposure to different investment styles

A sample portfolio could look like:

- 60% Index Funds (BOVA11, IVVB11, ETFs)

- 30% Active Funds (Multimercados, small-cap funds)

- 10% Cash or Tesouro Direto

Tax Considerations

In Brazil:

- ETFs and mutual funds are taxed differently.

- ETFs: Gains are taxed at 15% (long term), and you need to pay DARF manually.

- Mutual funds (fundos de investimento): Often have automatic IR collection, known as the “come-cotas” every 6 months.

Always consider net returns after taxes and fees, not just gross performance.

Key Takeaways

- Index Funds are ideal for cost-conscious, long-term investors who want to match market returns.

- Active Funds offer potential upside but come with higher fees and risk.

- Over long periods, index funds often outperform the majority of active funds.

- Consider using both in a diversified portfolio, depending on your goals and knowledge.

Final Verdict: Which Is Better?

There’s no one-size-fits-all answer, but here’s a general rule:

- For most people, especially beginners or those without time to research, index funds are the better, safer bet.

- For those who understand market cycles, risk management, and specific sectors, a carefully selected active fundcan add value.

The real winner? The investor who stays consistent, keeps fees low, diversifies properly, and stays invested over time— regardless of the fund type.